The Spring Ramp-Up Checklist: Financing Equipment Before Busy Season Hits

Beat the Busy-Season Crunch with Early Equipment Financing

Seasonal businesses do not get much room for error. Spring arrives quickly, and once demand starts building, the priority has to shift to doing the work, serving customers, and generating revenue. That leaves very little time to deal with delays, paperwork, or equipment problems that should have been handled earlier.

That’s why it helps to get ahead of the rush. In some cases, that means adding equipment to increase capacity, reduce downtime, replace something unreliable, or fix workflow issues that could slow your team down when business is at its busiest.

Blue Bridge Financial helps businesses like yours prepare for the busy season by financing equipment purchases before timing gets tight.

Define the upgrade and tie it to revenue

A busy season equipment upgrade should solve a real problem. It should help you take on more work, improve turnaround time, or cut down on lost hours caused by breakdowns and bottlenecks.

A good place to start is by identifying what’s holding you back today.

It may be a machine that’s become unreliable. It may be a truck that no longer fits the jobs you’re bidding. It may be the fact that one crew is waiting on another because you don’t have enough equipment to keep both moving.

Then put a number on the problem. If the equipment isn’t in place when demand picks up, what does that cost you in lost jobs, delays, rentals, overtime, or customer frustration?

That number tells you why the upgrade matters, and it helps keep the decision grounded in the realities of your business.

Map the timing, then work backward

A lot of seasonal businesses wait until the calendar is already filling up before they start shopping and applying for financing. That’s usually when timing becomes expensive.

A better approach is to work backward from when the equipment needs to be on-site and ready to use. When do jobs typically start stacking up? When does your team need the truck, trailer, or machine in hand? How long could quoting, sourcing, delivery, and setup realistically take?

Once you answer those questions, the financing timeline becomes easier to see. The point isn’t to apply as early as possible for the sake of it. The point is to apply early enough that financing doesn’t become the thing that holds up the purchase.

Waiting often means fewer options, less leverage, and more pressure to make a quick decision.

Get a clear vendor quote early

A vague estimate can slow everything down. A clear quote usually does the opposite, setting the stage for success. An approval from Blue Bridge lasts 60 days, which makes getting approved early helpful in your planning.

Before you apply, ask your vendor for a quote that covers the basics: what the equipment is, what it costs, and when it can be delivered. If the quote also includes the make, model, year, and serial number, even better.

Spring has a way of tightening inventories fast, and recent supply chain and tariff issues can add complexity. Equipment that is available today may not still be available next week. A complete quote makes it easier to move while the right unit is still on the table.

When timing matters and inventory is limited, used equipment can make a lot of sense. It helps to have your budget, paperwork, and timing lined up in advance so you are ready to move when a strong option becomes available.

Use a simple equipment financing checklist for your documents

You don’t need a huge packet. But it helps to have the basics organized so you are not tracking down information when the season is already getting busy.

Here is a practical checklist of information that lenders commonly want to review:

- Legal business name, address, and tax ID

- Ownership information

- Time in business

- Basic revenue snapshot, plus a quick note on seasonality

- Current obligations and monthly payments

- Vendor quote and equipment details

With Blue Bridge Financial, the initial process is often simpler than business owners expect. In many cases, a one-page application is enough to start the review, and additional items such as recent bank statements are only requested in some situations.

Build seasonal cash flow planning into the decision

Seasonal cash flow planning matters because a payment that feels manageable in your busiest months can feel very different in a slower stretch.

Before moving forward, take a look at the last two or three years and identify the months when cash tends to tighten. Then compare those periods with your baseline expenses, payroll, insurance, rent, fuel, and other operating costs.

This doesn’t need to become a complicated exercise. You’re really answering one practical question: will this payment still feel manageable when business is slower?

If the answer is no, or even maybe, it’s worth pausing and adjusting the plan before you commit.

Choose the right tool: equipment financing vs working capital

When things start moving quickly, it can be tempting to use whichever funding option seems fastest. But the fastest option isn’t always the one that fits the situation best.

If you’re purchasing a long-life asset, equipment financing usually makes more sense because the structure is designed around that kind of purchase. If you’re covering short-term gaps like payroll, operating expenses, or timing pressure while work ramps up, that is usually a working capital conversation instead.

Want a clear comparison? Here’s a breakdown of working capital vs equipment financing.

Using the right financing tool from the start can make payments more predictable and help reduce pressure on cash flow.

Decide what to finance, and what to keep in cash

Busy season ramp-up brings a familiar kind of pressure. Payroll grows. Fuel costs rise. Materials go up. Small problems get more expensive because every delay can ripple through the schedule.

That’s why many seasonal operators choose to finance their core revenue-producing assets and keep cash available for the operating expenses that rise with volume. It’s often the cleaner way to add capacity without draining reserves right before the season gets demanding.

It also helps prevent a long-term equipment need from turning into a short-term cash problem.

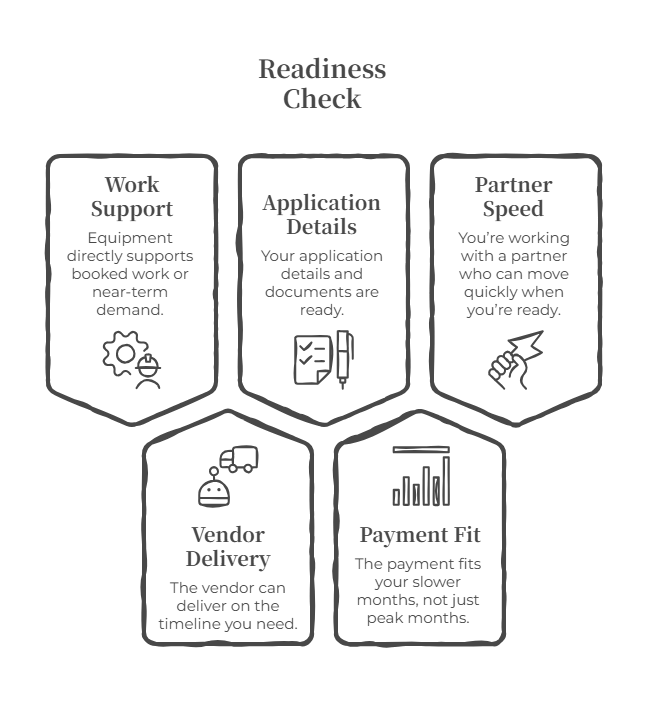

Use a five-point readiness check before you commit

Before you move ahead, take a minute to confirm the basics:

- The equipment directly supports booked work or near-term demand

- The vendor can deliver on the timeline you need

- Your application details and documents are ready

- The payment fits your slower months, not just peak months

- You’re working with a partner who can move quickly when you’re ready

If those boxes are checked, you’re in a much better position to move forward with confidence.

Start your spring equipment financing plan now

Spring demand won’t wait for approvals. Businesses that handle busy season well are usually the ones that got ready before the pressure started building.

Start your application today or contact Blue Bridge Financial to discuss equipment financing options tailored to your business needs and seasonal timing.